Real estate is one of the most common alternative assets investors use inside self-directed IRAs.

The appeal is clear: real estate may produce rental income, may appreciate over time, and gives investors exposure to a tangible asset class outside traditional stocks and bonds.

But the tax advantages only apply when the IRA owns the property outright, all income and expenses stay within the account, and the investor avoids prohibited transactions.

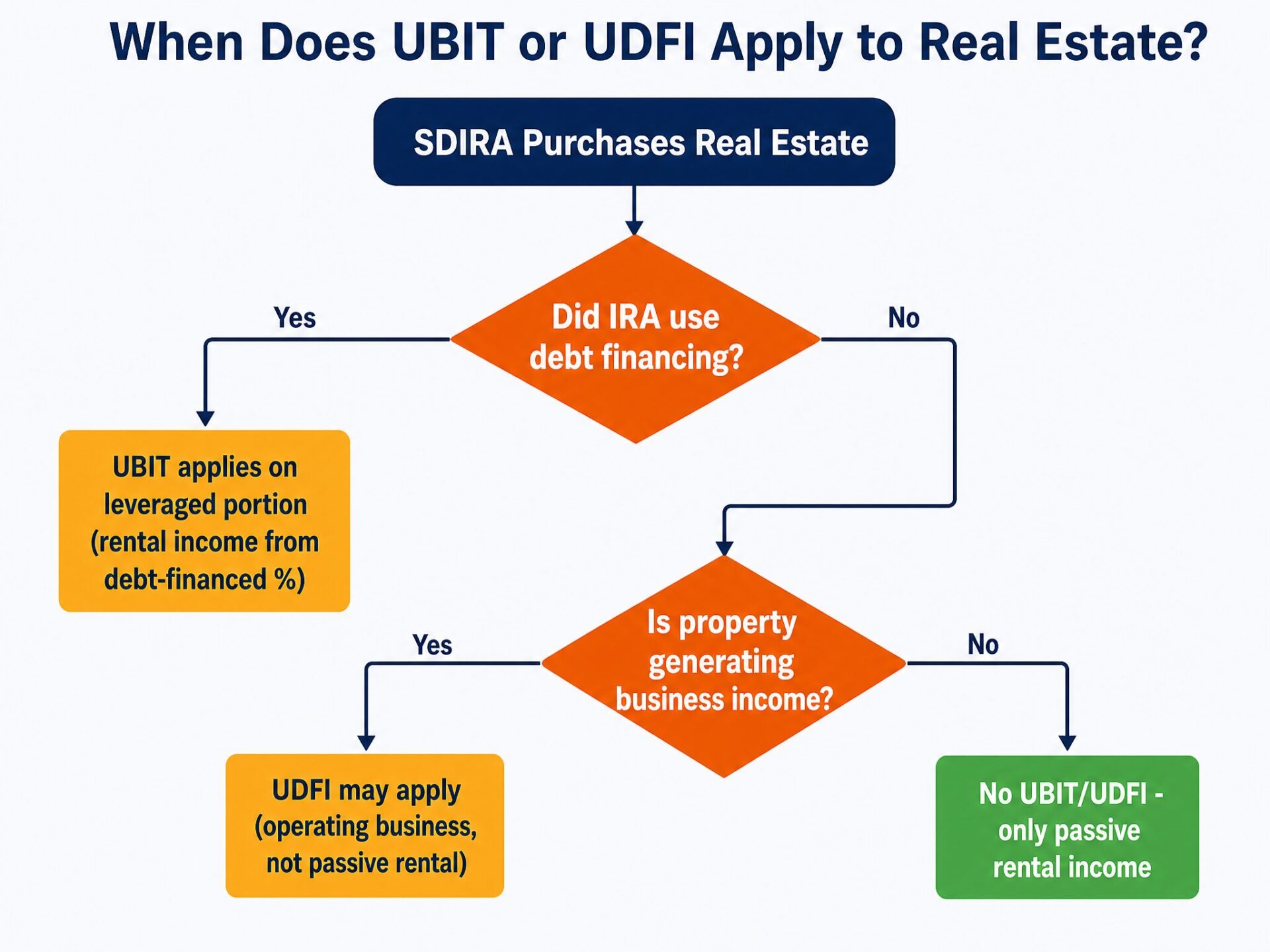

When you hold real estate inside a self-directed IRA, the benefits multiply. Rental income and gains generally flow back into the IRA tax-deferred in a Traditional IRA and may ultimately be tax-free in a Roth IRA if Roth-qualified distribution rules are met. Debt-financed real estate may create UBIT/UDFI.

You are building wealth on two fronts: the property appreciates while the tax savings compound.

I have personally overseen more than $1.4 billion in real estate and financial transactions. I have watched investors turn modest IRA balances into seven-figure portfolios using real estate. I have also watched people destroy their accounts by ignoring the rules.

This guide covers everything you need to know to invest in real estate with your self-directed IRA the right way.

Why Real Estate Is the Most Popular Self-Directed IRA Investment

Real estate dominates self-directed IRA portfolios for several compelling reasons.

First, it is a tangible asset. Unlike stocks or crypto, you can drive by your investment, inspect it, and insure it. That physical nature provides a level of security that paper assets cannot match.

Second, real estate generates dual returns. You earn rental income (cash flow) while the property appreciates in value. Inside a self-directed IRA, both streams grow tax-deferred or tax-free depending on your account type.

Third, real estate provides inflation protection. As prices rise, so do rents and property values. Your IRA’s purchasing power is preserved and enhanced.

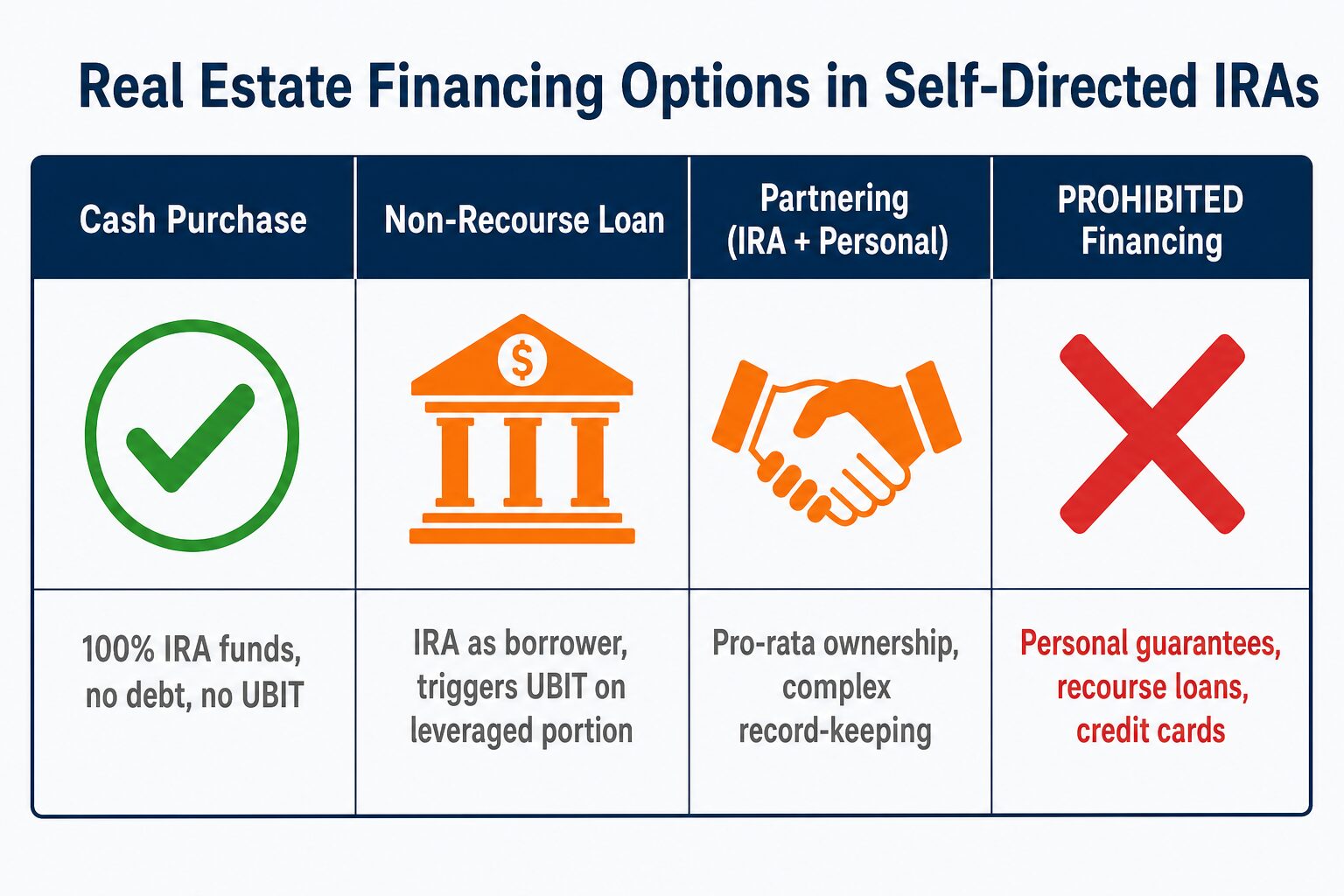

Fourth, you can leverage real estate. Using non-recourse loans, your IRA can control more property than its cash balance alone would allow. This amplifies returns significantly.

Finally, real estate offers predictable income. A well-chosen rental property in a strong market generates monthly cash flow that compounds inside your IRA year after year. Learn more about top IRA real estate investment strategies for building massive wealth.

Types of Real Estate You Can Buy with a Self-Directed IRA

The IRS does not limit SDIRA real estate to one specific property type, but the investment must avoid prohibited assets, prohibited transactions, personal use, and any structure that your custodian will not administer.

Here are the most common categories.

Residential Rental Properties

Single-family homes, duplexes, triplexes, and fourplexes are the most popular starting point. Your IRA purchases the property, collects rent, and all income returns to the account. This is straightforward, predictable, and scalable.

Commercial Real Estate

Office buildings, retail spaces, warehouses, and industrial properties. These often come with longer lease terms and higher rental yields than residential. Your IRA can own commercial property outright or as part of a partnership.

Multi-Family Apartment Buildings

Apartment complexes with five or more units. These require more capital but generate significant cash flow. Many investors pool IRA funds with partners to acquire larger multi-family assets. Learn how real estate syndication can help you access larger deals.

Raw Land

Undeveloped land is a legitimate IRA investment. Your IRA can purchase raw land and hold it for appreciation, or develop it (using IRA funds and third-party contractors only). Raw land has no tenants, no maintenance headaches, and no property management fees.

Fix-and-Flip Properties

Your IRA can purchase distressed properties, renovate them using IRA funds and independent contractors, and sell them for a profit. All gains stay in the IRA. But be aware: frequent flipping may trigger Unrelated Business Income Tax (UBIT). More on that below.

Real Estate Syndications

Your IRA can invest as a limited partner in real estate syndications and private placements. This gives you access to large commercial deals, apartment complexes, and development projects without managing the property yourself.

Real Estate Notes and Mortgages

Your IRA can act as the lender. Purchase existing mortgage notes or originate new loans to borrowers. The interest payments flow back into your IRA tax-deferred or tax-free. This is a popular strategy for investors who want real estate exposure without property management responsibilities.

FAQs

Can I buy real estate with my IRA?

Yes. A self-directed IRA allows you to purchase real estate directly. You can buy residential rentals, commercial properties, raw land, REITs, tax liens, and more. The property must be held for investment purposes only, not personal use.

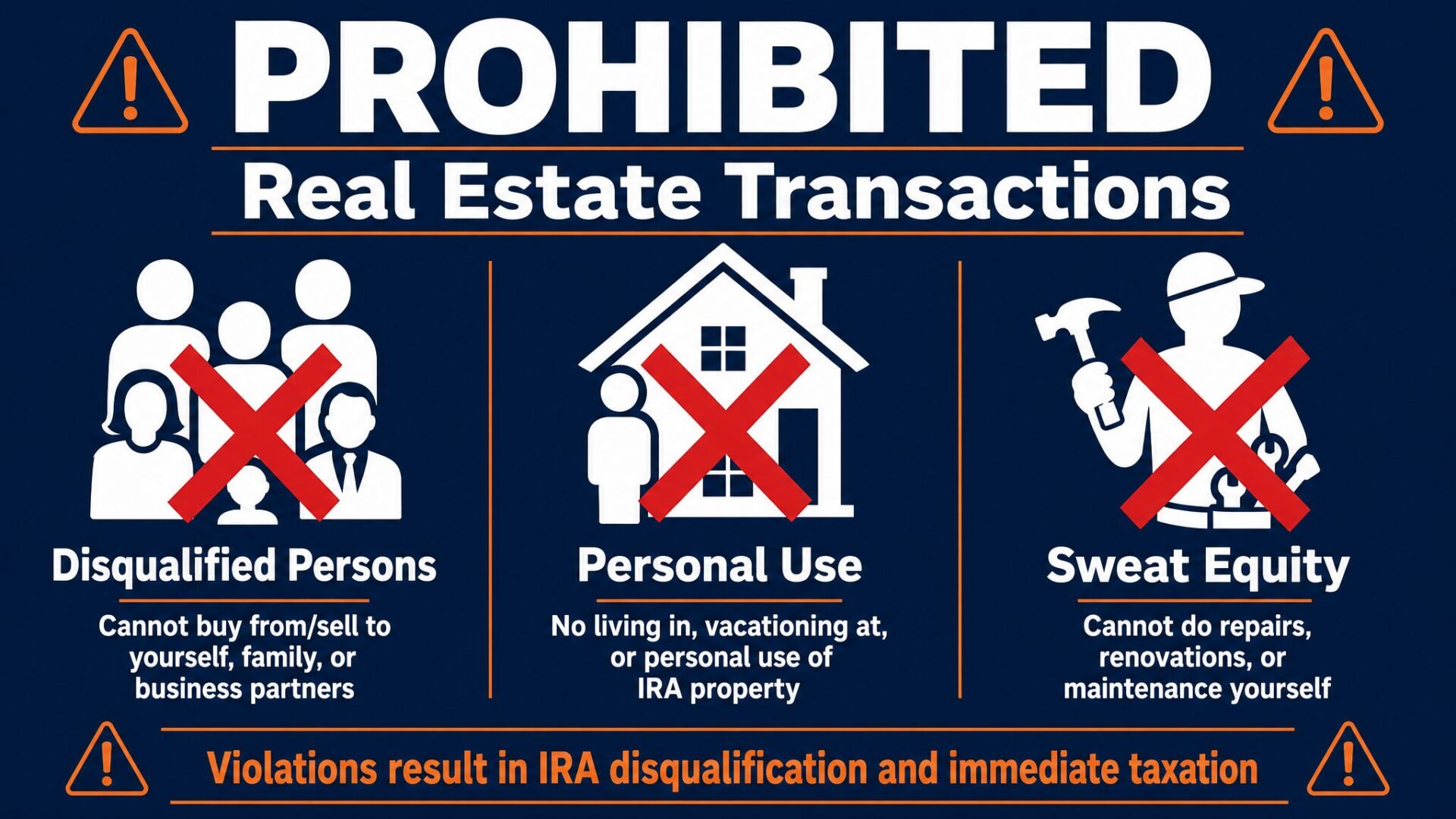

Can I live in a property owned by my self-directed IRA?

No. IRS rules prohibit you and disqualified persons (spouse, parents, children, their spouses) from living in, vacationing at, or personally using any property owned by your IRA. This is considered a prohibited transaction and can disqualify your entire IRA.

What is a non-recourse loan and why do I need one?

IRA-owned real estate financing generally must be non-recourse, meaning neither you nor another disqualified person may personally guarantee the loan or pledge personal assets. With this loan, the lender can only seize the property itself if you default. They cannot go after other IRA assets or your personal assets. Traditional mortgages are prohibited because they require personal guarantees.

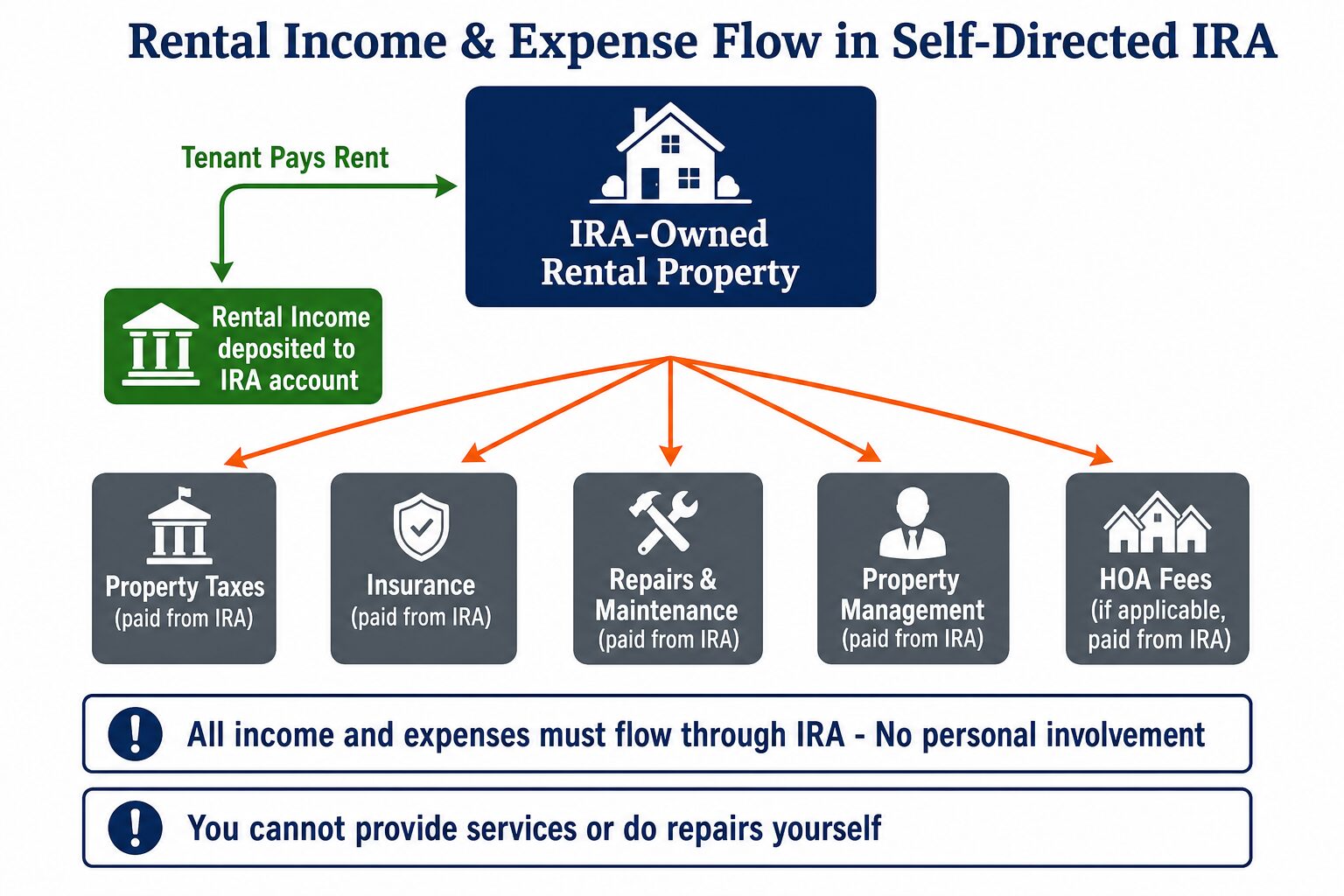

Can I manage the property myself or do repairs?

No. You may direct the IRA’s investment decisions, but you should not personally perform repairs, tenant services, rent collection, bookkeeping, maintenance, or property-management labor. Use IRA funds to pay independent third parties.

Where does rental income go?

All rental income must flow directly back into your IRA. You cannot deposit it into your personal bank account, even temporarily. The income grows tax-deferred (Traditional IRA) or tax-free (Roth IRA) inside the account.

What is UBIT and when does it apply?

UBIT (Unrelated Business Income Tax) applies when your IRA earns income from an active business or uses debt financing. If you buy real estate with a non-recourse loan, the leveraged portion of rental income may be subject to UBIT. Cash purchases typically avoid UBIT.

Can I flip houses in my self-directed IRA?

Yes, but be cautious. Frequent flipping can trigger UBIT because the IRS may classify it as dealer activity (active business income) rather than investment income. An occasional resale may be less likely to create UBIT than a regular flipping business, but the analysis is fact-specific. Review the strategy with a tax professional before using an IRA for repeated flips.

Can I partner with my IRA to buy property?

Possibly, but this is a high-risk structure that should be reviewed before closing. If personal funds and IRA funds co-invest, ownership, income, expenses, debt, and control must be structured carefully and proportionally, and later transactions between you and the IRA can create prohibited transaction issues.

What happens if I accidentally use the property personally?

Any personal use constitutes a prohibited transaction. The IRS can disqualify your entire IRA, treating the full account balance as a taxable distribution. You will owe income taxes and potentially a 10% early withdrawal penalty if you are under 59.5 years old. There is no safe personal-use allowance. Even brief personal use can create a prohibited transaction and may cause the IRA to be treated as distributed as of the first day of that tax year.

Can I buy property from or sell property to a family member?

No. You cannot buy from or sell to disqualified persons, including your spouse, parents, children, grandparents, grandchildren, and their spouses. You also cannot buy from entities controlled by disqualified persons. Siblings, aunts, uncles, and cousins are generally allowed.

How do I take distributions from real estate in my IRA?

You have three options: (1) Sell the property and distribute cash, (2) Take an in-kind distribution where the property title transfers to you personally (taxable event based on property value), or (3) Take periodic cash distributions from rental income if your IRA has sufficient liquidity.

What are the biggest mistakes people make with real estate IRAs?

The most common mistakes include: using the property personally, doing repairs yourself, commingling personal and IRA funds, buying from disqualified persons, personally guaranteeing loans, and failing to understand UBIT. Each of these can trigger severe tax penalties or IRA disqualification.