A self-directed IRA is a retirement account that lets you invest in assets far beyond the stocks, bonds, and mutual funds offered by traditional brokerages.

Real estate. Private equity. Precious metals. Tax liens. Promissory notes. Cryptocurrency. These are all on the table.

The IRS does not actually use the term “self-directed IRA.” Every IRA is technically self-directed. But the industry uses this label to describe accounts held with specialized custodians who allow alternative investments. Your standard Fidelity or Schwab account will not let you buy a rental property inside your IRA. A self-directed IRA custodian, such as Horizon Trust, will.

Here is the critical distinction: with a self-directed IRA, you are in the driver’s seat. The custodian does not give you investment advice. They do not vet your deals. They hold the assets, handle the paperwork, and ensure the account stays compliant with IRS rules. Every investment decision is yours.

I have spent decades in this space. I have watched investors build generational wealth using self-directed strategies. I have also watched people blow up their accounts by ignoring the rules. This guide covers everything you need to know to do it right.

Types of Self-Directed IRAs

A self-directed IRA is not a separate account type. It is a standard IRA held with a custodian that permits alternative investments. The tax treatment depends on which IRA structure you choose.

Traditional Self-Directed IRA

Contributions may be tax-deductible. Earnings grow tax-deferred. You pay taxes when you withdraw funds in retirement. Required Minimum Distributions (RMDs) begin at age 73.

Best for investors who expect to be in a lower tax bracket during retirement. Learn more about strategies to minimize your tax burden.

Roth Self-Directed IRA

Contributions are made with after-tax dollars. No upfront deduction. But qualified withdrawals in retirement are completely tax-free. No RMDs during the original owner’s lifetime.

Best for investors who expect higher future tax rates or want tax-free income in retirement. This is one of the most powerful wealth-building tools available. A Roth self-directed IRA holding appreciating real estate or private equity can generate substantial tax-free gains over decades. Explore our list of the best tax-free investments to build wealth.

SEP Self-Directed IRA

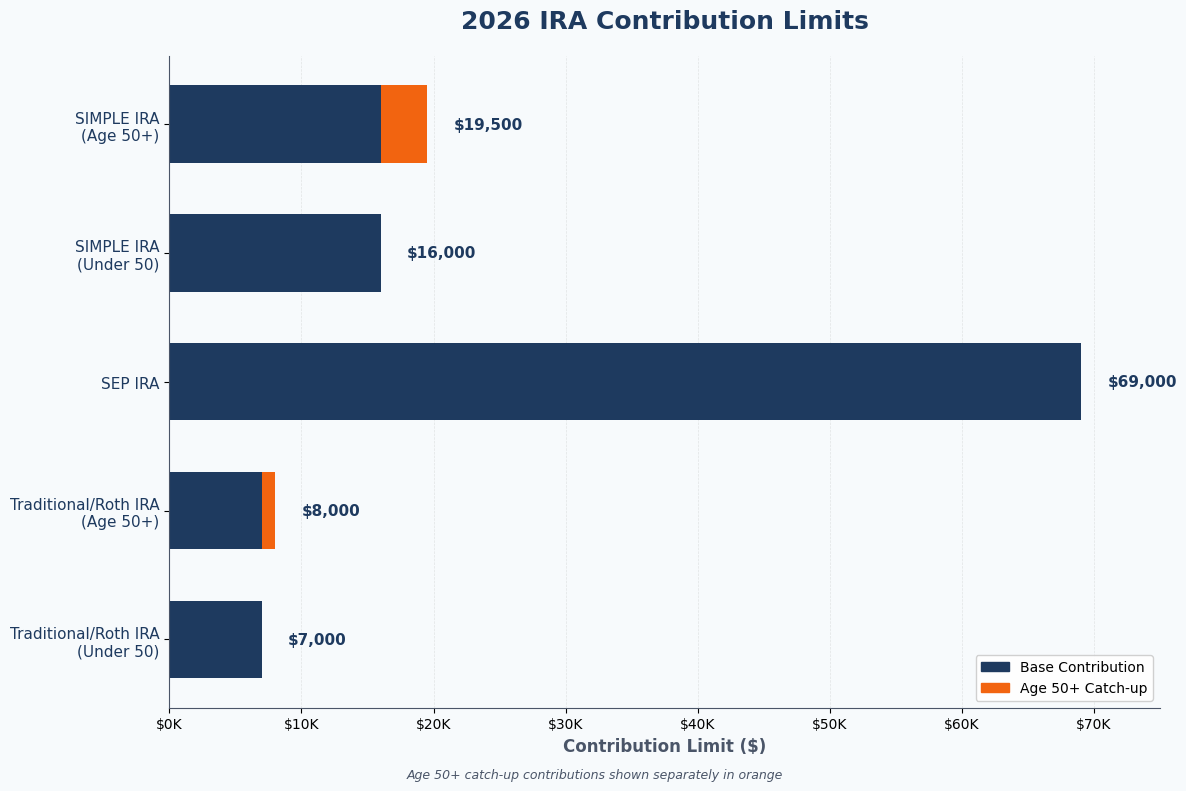

Designed for self-employed individuals and small business owners. Contributions are tax-deductible and grow tax-deferred. The 2026 contribution limit is up to 25% of compensation, with a maximum of $72,000. Contributions are discretionary, so you can adjust based on business performance.

Best for high-earning entrepreneurs who want to shelter significant income while investing in alternatives. See our guide to the best retirement accounts for self-employed individuals.

SIMPLE Self-Directed IRA

Built for small businesses with 100 or fewer employees. Allows both employee salary deferrals and mandatory employer contributions. The 2026 elective deferral limit is $17,000, with a $4,000 catch-up contribution for those 50 and older.

Best for small business owners who want a straightforward retirement plan with alternative investment options.

What You Can Invest In

This is where self-directed IRAs get interesting. The IRS does not provide a list of “approved” investments. Instead, it tells you what you cannot invest in. Everything else is fair game.

Real Estate

This is the most popular alternative investment in self-directed IRAs. For a deeper dive, read our guide to self-directed IRA real estate investing. Your IRA can purchase:

- Residential rental properties

- Commercial real estate

- Raw land

- Fix-and-flip projects

- Real estate syndications

- Real estate notes and mortgages

All rental income flows back into the IRA tax-deferred (Traditional) or tax-free (Roth). When the property sells, the gains stay in the account under the same tax treatment.

One critical rule: your IRA owns the property, not you. You cannot live in it. You cannot vacation in it. Your family members cannot use it. All expenses must be paid from IRA funds, and all income must return to the IRA. For proven approaches, explore top IRA real estate investment strategies for building massive wealth.

Private Equity and Private Placements

Your self-directed IRA can invest in startups, pre-IPO companies, private funds, and business ventures. This gives you access to opportunities that most retirement investors never see.

Precious Metals

Physical gold, silver, platinum, and palladium are permitted. But they must meet IRS purity standards. Gold must be 99.5% pure. Silver must be 99.9% pure. The metals must be stored with an IRS-approved depository. You cannot keep them in your home safe.

Private Lending and Promissory Notes

Your IRA can act as the bank. You lend money to borrowers and collect interest payments that flow back into your account. This includes real estate notes, business loans, and personal loans to non-disqualified persons.

Tax Liens and Tax Deeds

Your IRA can purchase tax lien certificates at county auctions. These can yield attractive interest rates, and in some cases, the IRA may acquire the underlying property. Our tax lien investing how-to guide covers this strategy in detail.

Cryptocurrency

Bitcoin, Ethereum, and other digital assets can be held in a self-directed IRA through specialized custodians. This is a growing category, though it carries significant volatility risk.

Other Permitted Investments

- LLCs and partnerships

- Foreign currencies

- Water rights

- Farmland

- Oil and gas interests

- Structured settlements

What You Cannot Invest In

The IRS explicitly prohibits three categories of investments inside any IRA:

Life Insurance

Your IRA cannot purchase life insurance policies. Period.

Collectibles

This includes artwork, antiques, rugs, gems, stamps, alcoholic beverages, and most coins. There are narrow exceptions for certain U.S. minted coins and IRS-approved bullion that meets purity standards.

S-Corporation Stock

IRAs cannot be shareholders in S-Corporations. Holding S-Corp stock in an IRA would cause the entity to lose its S-Corp tax status.

Prohibited Transactions: The Rules That Matter Most

This is where most people get into trouble. Understanding self-directed IRA rules and prohibited transactions is essential. The IRS has strict rules about how your self-directed IRA can interact with you and your family. Violate these rules and the consequences are severe.

The Exclusive Benefit Rule

Your IRA must exist solely for the benefit of your retirement. Any transaction that provides a direct or indirect personal benefit to you or a “disqualified person” before retirement is prohibited under IRC Section 4975.

Who Are Disqualified Persons?

- You (the account holder)

- Your spouse

- Your parents and grandparents

- Your children and grandchildren (and their spouses)

- Any fiduciary or service provider to the IRA

- Any entity where you or other disqualified persons hold 50% or more ownership

What You Cannot Do

- Buy property from or sell property to your IRA

- Rent IRA-owned property to yourself or family members

- Live in or vacation at IRA-owned real estate

- Perform maintenance or repairs on IRA-owned property (even for free)

- Lend money to or borrow money from your IRA

- Use IRA assets as collateral for a personal loan

- Pay yourself a salary for managing IRA investments

- Hire your children to work on IRA-owned properties

The Consequences

If you commit a prohibited transaction, the IRS treats your entire IRA as distributed on January 1 of the year the violation occurred. That means:

- The full account balance becomes taxable income

- A 10% early withdrawal penalty applies if you are under 59½

- Potential additional interest and penalties on unpaid taxes

I have seen investors lose six and seven figures because they did not understand these rules. Do not let that be you.

Benefits and Advantages of Self-Directed IRAs

True Portfolio Diversification

Wall Street wants you to believe diversification means owning different mutual funds. Real diversification means holding assets that do not move in lockstep with the stock market. Real estate, private equity, and precious metals provide genuine portfolio protection.

Higher Return Potential

Alternative investments can significantly outperform traditional market returns. Learn how self-directed IRAs work to unlock these opportunities. A well-chosen rental property or private equity deal inside a Roth IRA can generate tax-free returns that dwarf what the S&P 500 delivers.

Tax-Advantaged Growth

Every dollar of rental income, every capital gain, every interest payment grows tax-deferred or tax-free inside your IRA. Over 20 or 30 years, the compounding effect is enormous. Discover additional ways to avoid capital gains tax on your investments.

Control Over Your Retirement

You are not at the mercy of fund managers or market volatility. You choose the investments. You perform the due diligence. You control the outcome.

Asset Protection

IRA assets receive significant creditor protection under federal law (ERISA and the Bankruptcy Abuse Prevention Act). The specifics vary by state, but your retirement assets are generally shielded from lawsuits and creditors.

Generational Wealth Building

A Roth self-directed IRA can be passed to beneficiaries who receive the assets tax-free (subject to the 10-year distribution rule under the SECURE Act). This is one of the most powerful wealth transfer strategies available. Greg Herlean has helped investors implement these strategies for over three decades.

Rules and Regulations You Must Know

Contribution Limits (2026)

| Account Type | Under 50 | Age 50+ |

|---|---|---|

| Traditional/Roth IRA | $7,500 | $8,600 |

| SEP IRA | Up to 25% of comp (max $72,000) | Same |

| SIMPLE IRA | $17,000 | $21,000 |

Income Limits for Roth IRA Contributions

Roth IRA contributions are subject to income phase-outs. High earners may need to use a “backdoor Roth” strategy. Consult a tax professional for current thresholds.

Required Minimum Distributions

Traditional, SEP, and SIMPLE IRAs require RMDs beginning at age 73. Roth IRAs do not require RMDs during the original owner’s lifetime.

Annual Fair Market Valuation

You must provide your custodian with an annual fair market value (FMV) for every alternative asset in your IRA. This is reported on IRS Form 5498. For real estate, this typically requires an independent appraisal or broker price opinion.

UBIT and UDFI Taxes

Two taxes can apply to self-directed IRA investments:

Unrelated Business Income Tax (UBIT): If your IRA earns income from an active trade or business, that income may be subject to UBIT. This is reported on IRS Form 990-T, and the tax is paid by the IRA itself.

Unrelated Debt-Financed Income (UDFI): If your IRA uses leverage (a non-recourse loan) to purchase an asset like real estate, a portion of the income attributable to the borrowed funds may be subject to UDFI.

These taxes do not eliminate the benefits of self-directed investing. But you need to understand them and plan accordingly.

How to Open a Self-Directed IRA

Step 1: Choose a Custodian

Select a custodian that specializes in self-directed accounts and alternative investments. Look for:

- Experience and track record

- Fee transparency

- Range of permitted investments

- Technology and reporting capabilities

- Responsiveness and customer service

Do not choose based on fees alone. Learn more about Horizon Trust Company and what to look for in a custodian. A custodian that saves you $50 per year but delays your transactions by weeks will cost you far more in missed opportunities.

Step 2: Open and Fund the Account

You can fund your self-directed IRA through:

- Direct contribution: New money within annual limits

- Transfer: Moving funds from an existing IRA to your new custodian (trustee-to-trustee, no tax consequences)

- Rollover: Moving funds from a 401(k), 403(b), or other qualified plan (typically after leaving an employer). Read our guide on how to maximize your 401(k) when you leave a job

Transfers are the cleanest method. They happen directly between custodians with no tax implications and no time limits.

Step 3: Identify Your Investment

Perform thorough due diligence. Remember, the custodian will not evaluate your investment. That responsibility is entirely yours. Understand the asset, the market, the risks, and the expected returns.

Step 4: Direct the Investment

Submit an investment direction letter to your custodian. They will review it for compliance, process the paperwork, and execute the transaction on behalf of your IRA.

Step 5: Manage and Monitor

Track your investments. Ensure all income returns to the IRA. Pay all expenses from IRA funds. Provide annual valuations to your custodian.

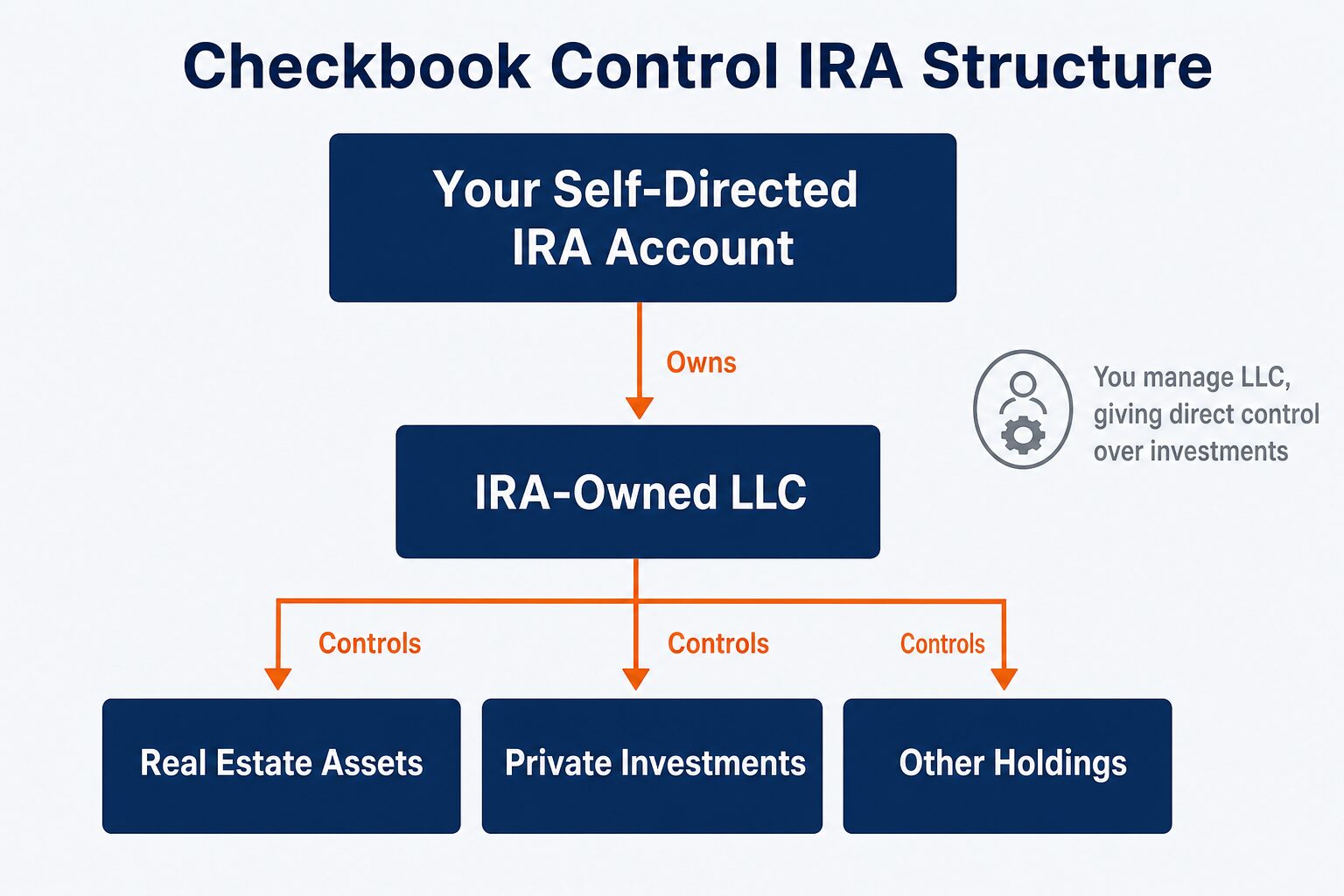

Checkbook Control IRA: Maximum Speed and Flexibility

A Checkbook Control IRA (also called an IRA LLC) is a structure that gives you direct transactional control over your retirement funds.

How It Works

- Your self-directed IRA forms and owns 100% of a new LLC

- You are designated as the manager of the LLC

- IRA funds are transferred to the LLC’s business checking account

- You write checks and execute transactions directly from that account

Why Investors Use It

Speed. You can write a check for an earnest money deposit at a real estate auction without waiting days for custodian approval.

Lower transaction costs. You avoid per-transaction fees charged by custodians for processing each investment.

Liability protection. The LLC structure can shield your IRA from liabilities associated with specific investments.

Privacy. Property titles and investments are held in the LLC’s name, not yours or the custodian’s.

The Compliance Reality

Checkbook control means checkbook responsibility. You must:

- Never commingle personal and IRA funds

- Never pay yourself for managing the LLC

- Maintain meticulous records

- Follow all prohibited transaction rules

- Provide annual valuations to your custodian

- File appropriate tax returns if the LLC has multiple members

This structure is powerful. But it is not for beginners. If you do not fully understand the prohibited transaction rules, a custodian-directed model is safer.

Common Mistakes to Avoid

Mistake 1: Self-Dealing

The number one killer of self-directed IRAs. Do not use IRA assets for personal benefit. Do not buy property from family members. Do not perform work on IRA-owned properties. The rules are strict and the IRS enforces them.

Mistake 2: Insufficient Due Diligence

Your custodian will not protect you from bad investments. Fraud exists in alternative investment markets. Verify everything. Get independent appraisals. Review financials. Consult professionals.

Mistake 3: Ignoring Liquidity Needs

Alternative investments are often illiquid. Real estate cannot be sold overnight. If you need to take an RMD and your only asset is a rental property, you have a problem. Maintain adequate liquidity in your account.

Mistake 4: Forgetting About Fees and Taxes

Custodian fees, LLC maintenance costs, UBIT, UDFI. These all eat into returns. Factor them into your investment analysis before committing capital.

Mistake 5: Not Getting Professional Help

Self-directed does not mean do-it-alone. Work with a tax advisor who understands self-directed IRAs. Work with an attorney who knows the prohibited transaction rules. The cost of professional guidance is a fraction of the cost of a compliance mistake. Contact us to discuss your self-directed IRA strategy.

Mistake 6: Failing to Provide Annual Valuations

Every alternative asset in your IRA must be valued annually. Failure to provide fair market valuations to your custodian can result in IRS penalties and compliance issues.

Mistake 7: Choosing the Wrong Custodian

Not all custodians are created equal. Some have limited investment options. Some have slow processing times. Some have hidden fees. Research thoroughly before committing.

Tax Implications: What You Need to Know

Traditional Self-Directed IRA

- Contributions may be tax-deductible

- All growth is tax-deferred

- Withdrawals in retirement are taxed as ordinary income

- Early withdrawals (before 59½) trigger a 10% penalty plus income tax

- RMDs begin at age 73

Roth Self-Directed IRA

- Contributions are not deductible

- All growth is tax-free

- Qualified withdrawals are completely tax-free

- No RMDs during the owner’s lifetime

- Five-year holding period applies for tax-free withdrawals

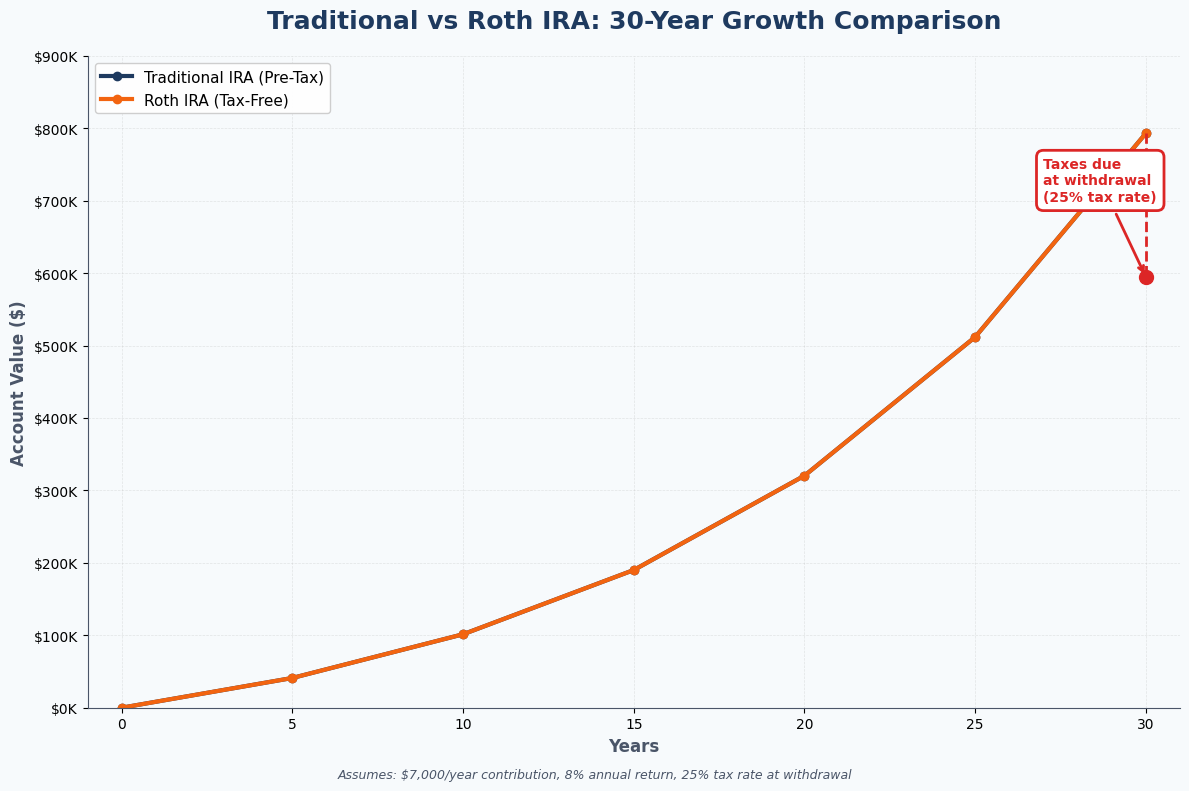

The Roth Conversion Strategy

Converting a Traditional self-directed IRA to a Roth triggers a taxable event. You pay income tax on the converted amount. But every dollar of future growth becomes tax-free. For investors with long time horizons and appreciating alternative assets, this strategy can save hundreds of thousands in lifetime taxes. Our tax-deferred vs. tax-free growth analysis breaks down the numbers.

UBIT and UDFI

As noted above, these taxes apply in specific situations. UBIT applies to active business income. UDFI applies to leveraged investments. Both are reported on Form 990-T and paid by the IRA. A knowledgeable tax advisor can help you structure investments to minimize these taxes.

Take Control of Your Retirement

A self-directed IRA is not for everyone. It requires knowledge, discipline, and a willingness to do the work that most investors avoid. But for those who commit to understanding the rules and performing proper due diligence, it is one of the most powerful wealth-building tools in existence.

I have spent over three decades helping investors use self-directed strategies to build real, lasting wealth. The opportunities are there. The tax advantages are extraordinary. The key is education.

Start with the fundamentals. Learn the rules. Build your team of advisors. Then take action. Download our free self-directed IRA and real estate investing eBooks to deepen your knowledge.

FAQs

Can I manage my own self-directed IRA investments?

Yes. That is the entire point. You choose the investments, perform due diligence, and direct the custodian to execute transactions. With a Checkbook Control IRA, you can execute transactions directly.

How much money do I need to open a self-directed IRA?

There is no IRS-mandated minimum. Custodian minimums vary. Some require as little as $0 to open an account. Others may require $5,000 or more. The practical minimum depends on your investment strategy. Real estate investments typically require more capital than promissory notes or tax liens. Our SDIRA real estate resource page can help you get started.

Can I invest in real estate I already own?

No. Purchasing property from yourself or a disqualified person is a prohibited transaction. Your IRA must acquire assets from unrelated third parties.

Can I use a self-directed IRA to invest in my own business?

Generally, no. Investing IRA funds in a business you own or control is considered self-dealing and constitutes a prohibited transaction.

What happens if I need money before retirement?

You can take distributions from your self-directed IRA, but early withdrawals (before age 59½) from a Traditional IRA are subject to income tax plus a 10% penalty. Roth IRA contributions (not earnings) can be withdrawn at any time without tax or penalty.

Is a self-directed IRA safe?

The account structure is governed by the same IRS rules as any other IRA. The safety of your investments depends entirely on your due diligence. The account itself is as safe as any IRA. The investments inside it carry whatever risk is inherent to the asset class.

Can I have multiple self-directed IRAs?

Yes. You can have multiple IRAs of different types. However, annual contribution limits apply across all your IRAs combined.

Do I need a special custodian?

Yes. Standard brokerages like Fidelity, Schwab, and Vanguard do not support alternative investments. You need a custodian that specializes in self-directed accounts.

What is the difference between a custodian and an administrator?

A custodian holds the assets and is regulated by federal or state banking authorities. An administrator facilitates transactions but may not hold assets directly. Some firms serve both functions. Always verify the regulatory status of your chosen provider.

How are self-directed IRA investments taxed when I withdraw?

Traditional IRA withdrawals are taxed as ordinary income. Roth IRA qualified withdrawals are tax-free. The type of investment inside the account does not change the tax treatment of distributions.

Disclaimer: This content is for educational purposes only and does not constitute investment, tax, or legal advice. Consult qualified professionals before making investment decisions. Greg Herlean is not a financial advisor, tax advisor, or attorney.